Quince: The Hottest One-Stop Dupe Shop

Quince: The Hottest One-Stop Dupe ShopCan a company built on $50 cashmere sweaters truly become the next Zara or Shein?Given the dearth of IPOs, I’m expanding the scope of my blog to include rapidly scaling private companies. Let’s start now with Quince, which may be the most interesting new ecommerce brand since SHEIN. Stay to the end, where I share the most important learnings for founders and investors. 1/ TL;DR on Quince: Solid Quality at Shocking Prices. Quince is reviving a classic retail strategy – selling uniquely supplied, high(ish)-quality goods at low prices – and doing it in the era of Instagram and TikTok. It’s a back-to-basics idea supercharged by modern distribution. If Quince continues executing with high margins, product innovation, and customer delight, it has a real shot at joining the pantheon of great American value retailers. 2/ There is a long list of retail legends that simply sell more for less. It starts with Sears Roebuck and progresses to Walmart, including big-box, category-specific retailers like Home Depot and Best Buy; club stores like Costco and Sam’s Club; off-price retailers like TJX; and fast-fashion brands like H&M, Uniqlo, and Zara (and most recently Shein). 3/ Quince may look different from the retail names that came before it, but it joins the tradition with its “affordable luxury” at bargain prices. 4/ How Quince Does It? Quince curates a network of global factories that produce for known brands like Theory and Away, then taps their excess capacity to manufacture similar products at standout prices, with factories holding the inventory and no middleman in sight. And their savvy approach goes beyond production facilities, showing up in their marketing and merchandising. 5/ Quince’s initial breakthrough was powered by the viral $50 cashmere sweater. The latest deal is Quince-branded Royal Osetra caviar tins for $125, far below comparable tins selling for $500 at retail. The team’s hero SKU-driven engagement playbook brings new customers in the door and keeps existing customers coming back. You may recognize this playbook via Costco’s $4.99 rotisserie chicken or Trader Joe’s “Two Buck Chuck.” 6/ The best businesses mirror a subscription, whether or not that’s their model. Quince drives repeat business by constantly growing its catalog – from 700 SKUs at launch in late 2020 to thousands now, spanning apparel, home, beauty, luggage, and more. 7/ Most of their products are “dupes” (a nice word for knock-offs) of brand name products: kids’ wear copying Hanna Andersson, coats echoing Theory, luggage mirroring Away. Quince proudly makes these comparisons on their website, highlighting the price differences. Everyone wins (except the higher-priced competitors). The factories get higher capacity utilization and Quince customers get lower prices. 8/ Why Customers Love Quince. Now is the value too good to be true? It depends on who you ask and how deep you dive into endless Reddit threads about the business. 9/ Ultimately, online reviews mean a lot less than U-shaped revenue retention curves. What does this mean? Well, after an initial group of customers try the product, the customers who come back spend more every quarter thereafter. We don’t have customer retention or cohort behavior from Quince, but based on talking to folks close to the company, Quince has been able to capture more share of wallet from its customers over time, further fueling growth. 10/ On the back of this maniacal customer love, Quince’s revenue reportedly doubled in 2024 to an estimated $675–700 million and SaaS database Latka has suggested a CAGR of >90% since 2020. It is now reportedly approaching a $2 billion run rate. 11/ Can Quince Economically Sustain Success? The company has long leaned into transparency on product detail pages. On the $50 cashmere crewneck, there is little to no SKU‑level margin—a classic, deliberate loss‑leader to earn traffic and trust, paid back via repeat purchases and basket expansion. As tariffs rise, you can expect to see ‘duties/taxes/fees’ having an impact —expect periodic pricing and routing adjustments to keep the value promise intact.

12/ Over time, Quince has smartly added higher-margin categories like vitamins and supplements, which has reportedly led the company to achieve gross margins in the 40s. There is a lot of room between Costco’s 12% gross margin and Zara’s 58%. Offering extreme value and vacuuming up customer share of wallet is far better than eking out every margin dollar. 13/ Reflecting all this upside, Quince recently raised at a greater than $4.5B valuation. There aren’t any reported plans for Quince to go public. So let’s speculate for a minute. Could Quince list at $10B+ if it goes public with $2 billion in trailing twelve month sales? If it maintains >50% growth with healthy contribution margins, a 5x sales multiple isn’t crazy in today’s market for premium growth stories. For example, TJX trades at a low‑single‑digit sales multiple, with On Holding in the mid-single digits. TL;DR for Founders. In this new section we will talk about lessons for earlier stage founder to take from companies that have achieved venture scale.

Any founders looking to build an ecommerce behemoth? Let’s chat. I’d love to find the next Quince! Ringing the Bell: A VC's Analysis of Consumer IPOs is free today. But if you enjoyed this post, you can tell Ringing the Bell: A VC's Analysis of Consumer IPOs that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|

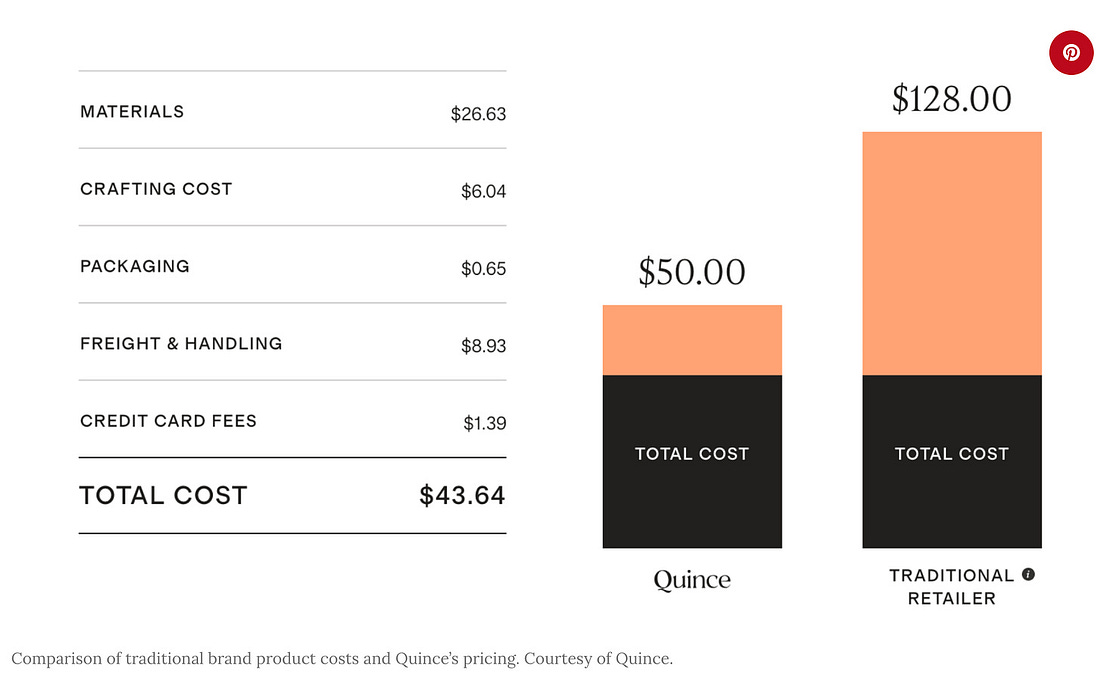

Views